This Bay view rental in Dennis has breath taking views! This 3 bedroom 3 bath home is located on Cape Cod Bay. The beautiful private sandy beach is perfect for relaxing on those warm summer days and going for a swim. The home is only a short walk to the Surf Side Grill on Corporation Beach. Enjoy magnificent sunsets right from your deck. It is only a short drive to golf, fishing and a wide selection of restaurants. Amenities include WiFi and a window a/c unit, not that you will need it with the refreshing summer sea breezes off of Cape Cod Bay! Additional amenities include: Outdoor Shower,Ceiling Fans, house phone, patio, deck furniture, dishwasher, microwave, lobster pot, blender, food processor, window a/c unit, coffee maker, vcr, dvd player, cable tv, iron, ironing board, vacuum, washing machine and dryer, a gas grill and other fans. If you are still looking for your Cape Cod Summer Vacation Getaway this home is for you! Call Foran Realty today for availability or visit the website at www.rentcapecodproperties.com and look for property PMA83. We look forward to helping you plan your Cape Cod Summer Vacation at this Bay view home!

The bottom line is clear….if you want to sell your home, don’t underestimate the role a real estate agent/broker can play in the process. They will be there to help you price the home, show the home, market the home and finally guide the seller through the offer, the purchase and sale and finally the closing. Having an agent/broker by your side has become crucial to the speed and efficiency in which your home can sell. Foran Realty can help! Foran Realty is a local Cape Cod real estate office that employs the latest in technology to help with the sale of your house. Call us today to find out how we can help you get your house sold!

The bottom line is clear….if you want to sell your home, don’t underestimate the role a real estate agent/broker can play in the process. They will be there to help you price the home, show the home, market the home and finally guide the seller through the offer, the purchase and sale and finally the closing. Having an agent/broker by your side has become crucial to the speed and efficiency in which your home can sell. Foran Realty can help! Foran Realty is a local Cape Cod real estate office that employs the latest in technology to help with the sale of your house. Call us today to find out how we can help you get your house sold!

increases through 2016’s quarters: Q1 4.4 percent; Q2 4.7 percent; Q3 4.9 percent; Q4 5.1 percent.

Fannie Mae however forecasts much smaller rises in current mortgage rates with forecasts much smaller and shallower rises, with only 4.2 percent in the last quarter of 2016. Q1, 4.1 percent in Q2 and 4.2 percent in both Q3 and Q4.

So Who’s Right?

So we know that both of these research teams are incredibly intelligent and the fact is either could be right (or both could be wrong). Even the Federal Reserve will not confidently predict when its own rates will rise, and it sets those itself.

Most experts and economists currently expect to see some rises between now and the end of 2016. However, a few reckon it could be a long time before we get back to normal levels. One, Deutsche Bank equity strategist David Bianco, wrote in early October, “We see a better chance of landing men on Mars before a full normalization of nominal and real interest rates, especially 10-year yields, to historical norms.”

What to Watch For

Usually, good economic data causes rates to rise, while poor numbers pull the rates down. In particular, low unemployment and inflation at around 2 percent are important, because those are the main criteria the Fed looks at when setting its rates. But good numbers regarding gross domestic product (GDP), incomes, manufacturing, consumer confidence and spending, and so on are all likely to see rates rise sooner and faster. Poor ones generally have the opposite effect, as does bad news about foreign economies. What happened in Greece this past year definitely helped to keep our rates low!

increases through 2016’s quarters: Q1 4.4 percent; Q2 4.7 percent; Q3 4.9 percent; Q4 5.1 percent.

Fannie Mae however forecasts much smaller rises in current mortgage rates with forecasts much smaller and shallower rises, with only 4.2 percent in the last quarter of 2016. Q1, 4.1 percent in Q2 and 4.2 percent in both Q3 and Q4.

So Who’s Right?

So we know that both of these research teams are incredibly intelligent and the fact is either could be right (or both could be wrong). Even the Federal Reserve will not confidently predict when its own rates will rise, and it sets those itself.

Most experts and economists currently expect to see some rises between now and the end of 2016. However, a few reckon it could be a long time before we get back to normal levels. One, Deutsche Bank equity strategist David Bianco, wrote in early October, “We see a better chance of landing men on Mars before a full normalization of nominal and real interest rates, especially 10-year yields, to historical norms.”

What to Watch For

Usually, good economic data causes rates to rise, while poor numbers pull the rates down. In particular, low unemployment and inflation at around 2 percent are important, because those are the main criteria the Fed looks at when setting its rates. But good numbers regarding gross domestic product (GDP), incomes, manufacturing, consumer confidence and spending, and so on are all likely to see rates rise sooner and faster. Poor ones generally have the opposite effect, as does bad news about foreign economies. What happened in Greece this past year definitely helped to keep our rates low!

What’s going to happen to current mortgage rates in 2016? The short answer is nobody can be sure. If you’re reading this because you need to make an important decision (time the purchase of a home, perhaps, or decide when to refinance an adjustable rate mortgage, we haven’t been much help. However we have given you the signs to watch for!

Rates now are still low so it is a great time to buy a home and lock yourself in at those low fixed rates. The team at Foran Realty would be happy to help you with your home search needs on Cape Cod.

What’s going to happen to current mortgage rates in 2016? The short answer is nobody can be sure. If you’re reading this because you need to make an important decision (time the purchase of a home, perhaps, or decide when to refinance an adjustable rate mortgage, we haven’t been much help. However we have given you the signs to watch for!

Rates now are still low so it is a great time to buy a home and lock yourself in at those low fixed rates. The team at Foran Realty would be happy to help you with your home search needs on Cape Cod.

Most people just want to be heard, first and foremost. Listening and responding appropriately to your client’s questions and or needs should always precede any recommendations or suggestions.

Most people just want to be heard, first and foremost. Listening and responding appropriately to your client’s questions and or needs should always precede any recommendations or suggestions.

never gets checked. If you are going to be unavailable be sure that someone else knows of the customers concerns and can address them should the need arise. The lesson to learn is to have live people answering phones, empowered to resolve problems. This goes for responses on your website as well. Be sure to make it easy for customers to access the “help” section of your site and then monitor it frequently enough to respond quickly.

never gets checked. If you are going to be unavailable be sure that someone else knows of the customers concerns and can address them should the need arise. The lesson to learn is to have live people answering phones, empowered to resolve problems. This goes for responses on your website as well. Be sure to make it easy for customers to access the “help” section of your site and then monitor it frequently enough to respond quickly.

purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

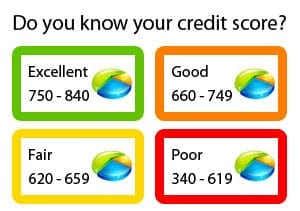

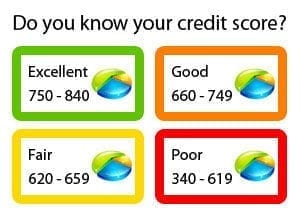

Strengthen Your Credit Score

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

Strengthen Your Credit Score

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years.

Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years. Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at:

Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at:  technology creating the ultimate experience for our customers, our growth has been consistently strong.

In 2015, Peter McDowell Associates of Dennis, MA merged with Foran Realty, and in 2016 Dubin Associates of East Dennis also joined forces with Foran Realty. Both McDowell Associates and Dubin Associates have deep roots in the mid-Cape Real Estate community and recognized the value Foran Realty brought to its Clients and both Principals wanted to become part of our exciting future.

Patrick works with each agent in the office to help them achieve their individual goals. Our Client centric culture removes competition from our office, and all of our agents work together and help each other succeed in our colloquial work environment.

We are currently looking to add a few select professionals to our Team. We are most selective in who we bring onto our Team, as we want to be certain our culture and Client focus remain intact. Unlike other real estate firms (especially the franchises and “box” firms), we do not hire everyone who walks through our door! Our agents must be Client focused, self-starting, tech savvy, able to resolve problems and satisfactorily address challenges, and also be a “people person” who loves his or her career and interacting with people.

Foran Realty offers an attractive compensation package, with no hidden fees. Foran Realty also offers a great referral program to select licensed agents who do not want to be involved in day to day business activities, but still want to earn commissions.

We offer progressive commission splits, free office space and each agent has access to a computer. We also provide the most up to date professional training and office technology.

If you feel your experience, talent and vision match our Culture of Excellence and you are considering a change for self-improvement and desire the opportunity to become an integral part of a locally owned growing firm, please forward a letter of introduction along with your resume to

technology creating the ultimate experience for our customers, our growth has been consistently strong.

In 2015, Peter McDowell Associates of Dennis, MA merged with Foran Realty, and in 2016 Dubin Associates of East Dennis also joined forces with Foran Realty. Both McDowell Associates and Dubin Associates have deep roots in the mid-Cape Real Estate community and recognized the value Foran Realty brought to its Clients and both Principals wanted to become part of our exciting future.

Patrick works with each agent in the office to help them achieve their individual goals. Our Client centric culture removes competition from our office, and all of our agents work together and help each other succeed in our colloquial work environment.

We are currently looking to add a few select professionals to our Team. We are most selective in who we bring onto our Team, as we want to be certain our culture and Client focus remain intact. Unlike other real estate firms (especially the franchises and “box” firms), we do not hire everyone who walks through our door! Our agents must be Client focused, self-starting, tech savvy, able to resolve problems and satisfactorily address challenges, and also be a “people person” who loves his or her career and interacting with people.

Foran Realty offers an attractive compensation package, with no hidden fees. Foran Realty also offers a great referral program to select licensed agents who do not want to be involved in day to day business activities, but still want to earn commissions.

We offer progressive commission splits, free office space and each agent has access to a computer. We also provide the most up to date professional training and office technology.

If you feel your experience, talent and vision match our Culture of Excellence and you are considering a change for self-improvement and desire the opportunity to become an integral part of a locally owned growing firm, please forward a letter of introduction along with your resume to  vacation home is used. A beach cottage has different requirements than a mountain cabin. If you don’t live nearby or don’t want to do the work yourself, be sure to budget for a property manager like Foran Realty.

Opening A Vacation Home

When it’s time to visit your vacation home for the first time, or start renting it out for the season, you’ll need to get it ready. A ski chalet might require you to shovel snow and chop firewood, while a summer retreat by the shore might call for cleaning patio furniture and staining the deck.

Much depends on how well the house is maintained throughout the year. Opening your vacation home could be as easy as stocking the pantry, or if the house was neglected in the offseason, you could have multiple repairs on your hands.

A well-maintained vacation home shouldn’t take more than a day to get in shape for the season, assuming no major repairs are needed. Here are some typical opening chores:

vacation home is used. A beach cottage has different requirements than a mountain cabin. If you don’t live nearby or don’t want to do the work yourself, be sure to budget for a property manager like Foran Realty.

Opening A Vacation Home

When it’s time to visit your vacation home for the first time, or start renting it out for the season, you’ll need to get it ready. A ski chalet might require you to shovel snow and chop firewood, while a summer retreat by the shore might call for cleaning patio furniture and staining the deck.

Much depends on how well the house is maintained throughout the year. Opening your vacation home could be as easy as stocking the pantry, or if the house was neglected in the offseason, you could have multiple repairs on your hands.

A well-maintained vacation home shouldn’t take more than a day to get in shape for the season, assuming no major repairs are needed. Here are some typical opening chores:

]]>

]]>