Want to Save Money on Heating Bills?

The temperature is dropping and the heating bills are going up. Some quick and easy tips will have you saving money this winter on home heating bills.

1. Set your thermostat back. For every degree you set your thermostat back over eight hours, you’ll save about 1 percent on your heating bill each year.

2. Use a space heater. If you spend most of your time in one area of your home it is less expensive to use a space heater than turn up the heat in your entire home.

3. Open blinds during the day to let sun in. At dusk, close them to trap heat.

4. Inspect weather stripping around exterior doors. Replace old, cracked, or missing stripping.

5. If heat is escaping at your doors, attach a sweep to the bottom of the doors. Sweeps are flexible plastic strips that are easily screwed to door bottoms, and keep cold air out from below.

6. Fill gaps around windows with interior and exterior caulking. If cold air is coming in around the sashes, install appropriate weather stripping.]]>

The temperature is dropping and the heating bills are going up. Some quick and easy tips will have you saving money this winter on home heating bills.

1. Set your thermostat back. For every degree you set your thermostat back over eight hours, you’ll save about 1 percent on your heating bill each year.

2. Use a space heater. If you spend most of your time in one area of your home it is less expensive to use a space heater than turn up the heat in your entire home.

3. Open blinds during the day to let sun in. At dusk, close them to trap heat.

4. Inspect weather stripping around exterior doors. Replace old, cracked, or missing stripping.

5. If heat is escaping at your doors, attach a sweep to the bottom of the doors. Sweeps are flexible plastic strips that are easily screwed to door bottoms, and keep cold air out from below.

6. Fill gaps around windows with interior and exterior caulking. If cold air is coming in around the sashes, install appropriate weather stripping.]]>

Planning for Money Milestones

In the course of a lifetime people encounter many money milestones. It can be difficult at times to know what to do with our money when we go through significant changes in life. Here are some of the major money milestones people encounter:

Marriage: According to TheKnot.com, Americans spend an average of $27,000 on a wedding. So vow not to start off your marriage in debt. Curb spending on the big day by cutting expenses where possible.

Buying a Home: Experts recommend saving for a 20% down payment for a home. Make sure to shop for a home loan and plan to spend no more than 30% of your taxable income on housing.

Starting a Family: The average cost of raising a child is $235,000, not including college. Plan your household costs to increase 10 to 20% with the addition of a baby.

Getting a Divorce: Divorce is expensive. Build a team of professionals who are knowledgeable about the implications of divorce, you will need a lawyer, accountant and financial advisor.

Retirement: 56% of Americans ages 18 to 34 aren’t saving for retirement. Take advantage of your employer’s 401(k) or other sponsored retirement plan. A good plan is to save five percent of your income.

]]>

In the course of a lifetime people encounter many money milestones. It can be difficult at times to know what to do with our money when we go through significant changes in life. Here are some of the major money milestones people encounter:

Marriage: According to TheKnot.com, Americans spend an average of $27,000 on a wedding. So vow not to start off your marriage in debt. Curb spending on the big day by cutting expenses where possible.

Buying a Home: Experts recommend saving for a 20% down payment for a home. Make sure to shop for a home loan and plan to spend no more than 30% of your taxable income on housing.

Starting a Family: The average cost of raising a child is $235,000, not including college. Plan your household costs to increase 10 to 20% with the addition of a baby.

Getting a Divorce: Divorce is expensive. Build a team of professionals who are knowledgeable about the implications of divorce, you will need a lawyer, accountant and financial advisor.

Retirement: 56% of Americans ages 18 to 34 aren’t saving for retirement. Take advantage of your employer’s 401(k) or other sponsored retirement plan. A good plan is to save five percent of your income.

]]>

Credit Card Tips

Credit cards can be a great source of safety and convenience but they can also be trouble. Buy now and pay later can have serious consequences and lead to financial trouble.

So in order to stay financially fit it is important to use your credit cards wisely. Here are a few tips to help you make the most of your credit cards:

• This seems simple but pay off your balance every month in full. Interest charges on your credit card purchases can add up fast.

• If you do carry a balance, pay back as much as you can as quickly as possible. You don’t have to wait until the payment due date.

• Avoid using your credit card to withdraw cash or transfer money. Interest is charged on these transactions immediately.

• If you are considering a card with an annual fee, be sure that whatever reward or benefit you’re getting is worth the cost.

Bottom line stay within your budget. Only use credit cards for things you can afford. If you can’t afford it don’t buy it. You will be much happier without the new sweater when you have enough money to buy a new home.]]>

Credit cards can be a great source of safety and convenience but they can also be trouble. Buy now and pay later can have serious consequences and lead to financial trouble.

So in order to stay financially fit it is important to use your credit cards wisely. Here are a few tips to help you make the most of your credit cards:

• This seems simple but pay off your balance every month in full. Interest charges on your credit card purchases can add up fast.

• If you do carry a balance, pay back as much as you can as quickly as possible. You don’t have to wait until the payment due date.

• Avoid using your credit card to withdraw cash or transfer money. Interest is charged on these transactions immediately.

• If you are considering a card with an annual fee, be sure that whatever reward or benefit you’re getting is worth the cost.

Bottom line stay within your budget. Only use credit cards for things you can afford. If you can’t afford it don’t buy it. You will be much happier without the new sweater when you have enough money to buy a new home.]]>

Value in Home Remodeling

More and more homeowners are choosing to stay in their homes and remodel. Homeowners who stay in their homes will eventually sell their home so it is important to make sure to choose a remodeling project that will get a good return on investment. Homeowners will also want to make sure to choose the right project for their living situation. The following are some helpful hints and a guide to the values of home remodeling projects.

First, you will want to ask yourself a few questions before you begin:

What is your budget?

What is the reason behind the project? Are you looking for more space? Updates?

Are you trying to improve your quality of life?

Is the goal to create more value in your home?

If you are looking to get the most resale value from your remodeling project, Remodeling Magazine has published a survey on how much some projects can increase the value of your home.

Here are just a few popular projects and their values:

Garage Addition 63.7% increase

Home Office Remodel 43.6% increase

Roofing Replacement 62.9% increase

Window Replacement (vinyl) 71.2% increase

For a full list of projects and how much you can expect to recoup you can read the Remodeling Cost Value Report by Remodeling Magazine.

]]>

More and more homeowners are choosing to stay in their homes and remodel. Homeowners who stay in their homes will eventually sell their home so it is important to make sure to choose a remodeling project that will get a good return on investment. Homeowners will also want to make sure to choose the right project for their living situation. The following are some helpful hints and a guide to the values of home remodeling projects.

First, you will want to ask yourself a few questions before you begin:

What is your budget?

What is the reason behind the project? Are you looking for more space? Updates?

Are you trying to improve your quality of life?

Is the goal to create more value in your home?

If you are looking to get the most resale value from your remodeling project, Remodeling Magazine has published a survey on how much some projects can increase the value of your home.

Here are just a few popular projects and their values:

Garage Addition 63.7% increase

Home Office Remodel 43.6% increase

Roofing Replacement 62.9% increase

Window Replacement (vinyl) 71.2% increase

For a full list of projects and how much you can expect to recoup you can read the Remodeling Cost Value Report by Remodeling Magazine.

]]>

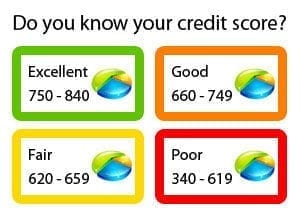

How to Raise Your Credit Score

If your credit score could use a boost it isn’t as simple as just changing bad financial behaviors. Increasing your credit score is a process that takes time. The time it takes to improve your credit history can vary.

Late payments can remain on your credit report for seven years, but typically if you clear all past-due debts and pay on time from then on, your score can begin to recover quickly.

One late payment doesn’t hurt you that much but a pattern of bad payments will really hurt you. If you have a few late payments continue to use credit and pay on time every time. Demonstrate that you are managing your fiances well and your scores will begin to climb.

If you have suffered a bankruptcy the effects can be long-lasting. According to myFico.com, a Chapter 13 bankruptcy can linger for seven to more than 10 years on your report. A Chapter 7 bankruptcy, or total liquidation, can affect your record for 10 years.

It is vital to constantly monitor your credit report and review it for accuracy. You can obtain your report for free once every twelve months from annualcreditreport.com.]]>

If your credit score could use a boost it isn’t as simple as just changing bad financial behaviors. Increasing your credit score is a process that takes time. The time it takes to improve your credit history can vary.

Late payments can remain on your credit report for seven years, but typically if you clear all past-due debts and pay on time from then on, your score can begin to recover quickly.

One late payment doesn’t hurt you that much but a pattern of bad payments will really hurt you. If you have a few late payments continue to use credit and pay on time every time. Demonstrate that you are managing your fiances well and your scores will begin to climb.

If you have suffered a bankruptcy the effects can be long-lasting. According to myFico.com, a Chapter 13 bankruptcy can linger for seven to more than 10 years on your report. A Chapter 7 bankruptcy, or total liquidation, can affect your record for 10 years.

It is vital to constantly monitor your credit report and review it for accuracy. You can obtain your report for free once every twelve months from annualcreditreport.com.]]>

Cool Yourself Without Air Conditioning

The warmer weather is here. If you don’t have air conditioning or just want to save money by not turning it on as often there are lots of ways to keep cool. So before you turn on the air or get overheated here are some tips on how to cool down your home as well as some tips for cooling yourself.

1. Keep the blinds shut

Keep the heat out by closing your blinds, curtains and windows during the day. This will block the sun’s heat. Keep everything shut until night falls and its cool enough to open the windows.

2. Open the windows

After nightfall open the windows to allow the cool night air to blow throughout house.

3. Use a fan

Place ceiling fans and window fans in upstairs rooms to draw off the heat and push the heat outdoors. Set up fans to suck up the cooler air from the floor below, and blow the hot air upwards towards the ceiling.

4. Create your own air conditioner

Believe it or not you can make your own air conditioner. Place a metal bowl of ice in front of a fan, and adjust the fan so that the air is blowing over the ice.

5. Avoid adding heat

Don’t add heat to your home especially during the day. Wait until the evening to take a hot shower, wash dishes and clothes or turn on the oven.]]>

The warmer weather is here. If you don’t have air conditioning or just want to save money by not turning it on as often there are lots of ways to keep cool. So before you turn on the air or get overheated here are some tips on how to cool down your home as well as some tips for cooling yourself.

1. Keep the blinds shut

Keep the heat out by closing your blinds, curtains and windows during the day. This will block the sun’s heat. Keep everything shut until night falls and its cool enough to open the windows.

2. Open the windows

After nightfall open the windows to allow the cool night air to blow throughout house.

3. Use a fan

Place ceiling fans and window fans in upstairs rooms to draw off the heat and push the heat outdoors. Set up fans to suck up the cooler air from the floor below, and blow the hot air upwards towards the ceiling.

4. Create your own air conditioner

Believe it or not you can make your own air conditioner. Place a metal bowl of ice in front of a fan, and adjust the fan so that the air is blowing over the ice.

5. Avoid adding heat

Don’t add heat to your home especially during the day. Wait until the evening to take a hot shower, wash dishes and clothes or turn on the oven.]]>

Save Money Insulating Your Home

Did you know that sealing and insulating your home is one of the most cost-effective ways to make a home more comfortable and energy efficient? It is a project that is also easily done yourself. The heating and cooling of your home accounts for about 50 percent to 70 percent of the energy used. So unless your home was built as an energy-efficient home, adding insulation will probably reduce your utility bills. Even a small amount of insulation-if properly installed-can reduce energy costs dramatically.

Energy Star has created a comprehensive do-it-yourself guide to sealing and insulating your home. The guide provides step by step instructions and photos to:

1.Learn how to find and seal hidden attic and basement air leaks

2.Determine if your attic insulation is adequate, and learn how to add more

3.Make sure your improvements are done safely

4.Reduce energy bills and help protect the environment

Click here to download the guide.

Make sure to check your state and local codes before starting any project and follow all safety precautions.]]>

Did you know that sealing and insulating your home is one of the most cost-effective ways to make a home more comfortable and energy efficient? It is a project that is also easily done yourself. The heating and cooling of your home accounts for about 50 percent to 70 percent of the energy used. So unless your home was built as an energy-efficient home, adding insulation will probably reduce your utility bills. Even a small amount of insulation-if properly installed-can reduce energy costs dramatically.

Energy Star has created a comprehensive do-it-yourself guide to sealing and insulating your home. The guide provides step by step instructions and photos to:

1.Learn how to find and seal hidden attic and basement air leaks

2.Determine if your attic insulation is adequate, and learn how to add more

3.Make sure your improvements are done safely

4.Reduce energy bills and help protect the environment

Click here to download the guide.

Make sure to check your state and local codes before starting any project and follow all safety precautions.]]>

Ready to be a homebuyer?

Have a checklist

Whether you are a 1st-time buyer or an experienced owner, buying a house requires a “preflight check,” in the words of Barry Zigas, director of housing policy for the Consumer Federation of America.

Read on for a checklist provided by Bankrate, including tips on the types of savings you need, plus advice about what matters beyond  purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

Strengthen Your Credit Score

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

Strengthen Your Credit Score

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

Higher scores wanted

Vicki Bott, a former official at the U.S. Department of Housing and Urban Development, says that her office noticed much the same thing. “While there are many qualified borrowers in the 580 range, the market today is probably looking for 640 to 660, at a minimum.” On the other end, a score of 700 to 720 will get you a good deal, and 750 and above will garner the best rates on the market. Improve your chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

Realistic debt-to-income ratio

For conventional loans, a safe formula is that home expenses should not exceed 28 percent of your gross monthly income, says Susan Tiffany, director of personal finance information for adults for the Credit Union National Association. Improve your chances by: trying on that financial obligation long before you sign the mortgage papers, says Tiffany. Before you home shop calculate the mortgage payment (there are several online calculators available) for the home in your intended price range, along with the increased expenses (such as taxes, insurance and utilities). Then bank the difference between that and what you’re paying now. Not only does it allow you to build a nice nest egg, but it gives you a feel for the comfort level in those payments. Once you have submitted your formal mortgage application, limit your spending to what is absolutely necessary. Do not make any substantial purchases and this could put your mortgage approval in jeopardy. Save for Down Payment and Closing Costs Depending on your credit and financing, you’ll typically need to save enough money for a down payment, somewhere between 3 percent and 20 percent of the home’s price.Don’t forget loan fees

Another substantial cash expense is your closing costs. Whatever your loan source, you’ll also need money to pay closing costs. For a $200,000 mortgage, closing costs run (depending on where you live) from $2,300 to $4,000. In a buyer’s market, you can also try to negotiate to have the seller pay a portion of the closing costs. Build a Healthy Savings Account Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years.

Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years. Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at: http://www.bankrate.com/finance/mortgages/]]>

Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at: http://www.bankrate.com/finance/mortgages/]]>

What to Ask Before You Add On

If you are thinking of adding an addition to your home there are some things you will wants to be aware of. If you decide to add a new space, ask yourself the following questions: * Can I finance the home improvement with my own cash or will I need a loan? * How much equity is in the property? A fair amount will make it that much easier to get a loan for home improvements. * Is it feasible to expand the current space for an addition? * What is permissible under local zoning and building laws? Despite your deep yearning for a new sunroom or garage, you will need to know if your town or city will allow such improvements. * Should I make the improvement myself or hire a contractor? Many homeowners consider going to job alone to save money. Consider how much time you have, your level of expertise or willingness to handle the job, amount of help from friends or relatives, and how much you want, or need, to save by doing the job yourself. You could save up to 20 percent of the project cost through your own hard work. Be aware, however, that you may need to call in the pros. Going it alone can sometimes lead to spending more time and money. if problems arise. Most home improvement experts suggest that homeowners who do not have a lot of experience should stick to painting, minor landscaping, building interior shelving, and other minor improvements.]]>