Credit cards can be a great source of safety and convenience but they can also be trouble. Buy now and pay later can have serious consequences and lead to financial trouble.

So in order to stay financially fit it is important to use your credit cards wisely. Here are a few tips to help you make the most of your credit cards:

• This seems simple but pay off your balance every month in full. Interest charges on your credit card purchases can add up fast.

• If you do carry a balance, pay back as much as you can as quickly as possible. You don’t have to wait until the payment due date.

• Avoid using your credit card to withdraw cash or transfer money. Interest is charged on these transactions immediately.

• If you are considering a card with an annual fee, be sure that whatever reward or benefit you’re getting is worth the cost.

Bottom line stay within your budget. Only use credit cards for things you can afford. If you can’t afford it don’t buy it. You will be much happier without the new sweater when you have enough money to buy a new home.]]>

Credit cards can be a great source of safety and convenience but they can also be trouble. Buy now and pay later can have serious consequences and lead to financial trouble.

So in order to stay financially fit it is important to use your credit cards wisely. Here are a few tips to help you make the most of your credit cards:

• This seems simple but pay off your balance every month in full. Interest charges on your credit card purchases can add up fast.

• If you do carry a balance, pay back as much as you can as quickly as possible. You don’t have to wait until the payment due date.

• Avoid using your credit card to withdraw cash or transfer money. Interest is charged on these transactions immediately.

• If you are considering a card with an annual fee, be sure that whatever reward or benefit you’re getting is worth the cost.

Bottom line stay within your budget. Only use credit cards for things you can afford. If you can’t afford it don’t buy it. You will be much happier without the new sweater when you have enough money to buy a new home.]]>

How to Raise Your Credit Score

If your credit score could use a boost it isn’t as simple as just changing bad financial behaviors. Increasing your credit score is a process that takes time. The time it takes to improve your credit history can vary.

Late payments can remain on your credit report for seven years, but typically if you clear all past-due debts and pay on time from then on, your score can begin to recover quickly.

One late payment doesn’t hurt you that much but a pattern of bad payments will really hurt you. If you have a few late payments continue to use credit and pay on time every time. Demonstrate that you are managing your fiances well and your scores will begin to climb.

If you have suffered a bankruptcy the effects can be long-lasting. According to myFico.com, a Chapter 13 bankruptcy can linger for seven to more than 10 years on your report. A Chapter 7 bankruptcy, or total liquidation, can affect your record for 10 years.

It is vital to constantly monitor your credit report and review it for accuracy. You can obtain your report for free once every twelve months from annualcreditreport.com.]]>

If your credit score could use a boost it isn’t as simple as just changing bad financial behaviors. Increasing your credit score is a process that takes time. The time it takes to improve your credit history can vary.

Late payments can remain on your credit report for seven years, but typically if you clear all past-due debts and pay on time from then on, your score can begin to recover quickly.

One late payment doesn’t hurt you that much but a pattern of bad payments will really hurt you. If you have a few late payments continue to use credit and pay on time every time. Demonstrate that you are managing your fiances well and your scores will begin to climb.

If you have suffered a bankruptcy the effects can be long-lasting. According to myFico.com, a Chapter 13 bankruptcy can linger for seven to more than 10 years on your report. A Chapter 7 bankruptcy, or total liquidation, can affect your record for 10 years.

It is vital to constantly monitor your credit report and review it for accuracy. You can obtain your report for free once every twelve months from annualcreditreport.com.]]>

Ready to be a homebuyer?

Have a checklist

Whether you are a 1st-time buyer or an experienced owner, buying a house requires a “preflight check,” in the words of Barry Zigas, director of housing policy for the Consumer Federation of America.

Read on for a checklist provided by Bankrate, including tips on the types of savings you need, plus advice about what matters beyond  purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

Strengthen Your Credit Score

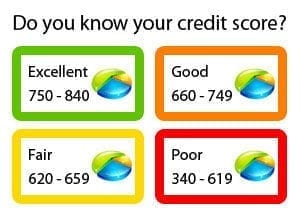

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

Strengthen Your Credit Score

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

Higher scores wanted

Vicki Bott, a former official at the U.S. Department of Housing and Urban Development, says that her office noticed much the same thing. “While there are many qualified borrowers in the 580 range, the market today is probably looking for 640 to 660, at a minimum.” On the other end, a score of 700 to 720 will get you a good deal, and 750 and above will garner the best rates on the market. Improve your chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

Realistic debt-to-income ratio

For conventional loans, a safe formula is that home expenses should not exceed 28 percent of your gross monthly income, says Susan Tiffany, director of personal finance information for adults for the Credit Union National Association. Improve your chances by: trying on that financial obligation long before you sign the mortgage papers, says Tiffany. Before you home shop calculate the mortgage payment (there are several online calculators available) for the home in your intended price range, along with the increased expenses (such as taxes, insurance and utilities). Then bank the difference between that and what you’re paying now. Not only does it allow you to build a nice nest egg, but it gives you a feel for the comfort level in those payments. Once you have submitted your formal mortgage application, limit your spending to what is absolutely necessary. Do not make any substantial purchases and this could put your mortgage approval in jeopardy. Save for Down Payment and Closing Costs Depending on your credit and financing, you’ll typically need to save enough money for a down payment, somewhere between 3 percent and 20 percent of the home’s price.Don’t forget loan fees

Another substantial cash expense is your closing costs. Whatever your loan source, you’ll also need money to pay closing costs. For a $200,000 mortgage, closing costs run (depending on where you live) from $2,300 to $4,000. In a buyer’s market, you can also try to negotiate to have the seller pay a portion of the closing costs. Build a Healthy Savings Account Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years.

Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years. Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at: http://www.bankrate.com/finance/mortgages/]]>

Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at: http://www.bankrate.com/finance/mortgages/]]>

How to Scare Off a Lender

You may think your credit is perfect because you pay your bills on time and never miss a payment. If you are having trouble getting a loan and don’t know why, it could be that your credit habits are scaring away lenders.

Here are some items that may be lurking in your credit report that are making lenders leery:

Multiple Lines of Credit

If you have a lot of open credit cards this can be a bad signal to lenders. Lenders see this as an indication that you might be having financial difficulty.

Credit Inquiries

Lenders also don’t like it when you inquire about new lines of credit. Applying for credit can have a negative impact on your credit score. Every time you allow a potential lender to pull up your credit report, your score can take a small hit.

Co-Signing a Loan

When you co-sign for a loan that dept becomes your debt and shows up on your credit report. Potential lenders look at that debt as yours because you are ultimately responsible for it. If the person you co-signed for stops paying, pays late, or misses payments, your credit report can be negatively impacted.

Making Minimum Payments

Lenders who view your credit report don’t like to see that you are paying just the minimum payment. If you consistently pay the minimum payment due, it could indicate financial stress or confirm that you are unable to pay off the full balance.

]]>

You may think your credit is perfect because you pay your bills on time and never miss a payment. If you are having trouble getting a loan and don’t know why, it could be that your credit habits are scaring away lenders.

Here are some items that may be lurking in your credit report that are making lenders leery:

Multiple Lines of Credit

If you have a lot of open credit cards this can be a bad signal to lenders. Lenders see this as an indication that you might be having financial difficulty.

Credit Inquiries

Lenders also don’t like it when you inquire about new lines of credit. Applying for credit can have a negative impact on your credit score. Every time you allow a potential lender to pull up your credit report, your score can take a small hit.

Co-Signing a Loan

When you co-sign for a loan that dept becomes your debt and shows up on your credit report. Potential lenders look at that debt as yours because you are ultimately responsible for it. If the person you co-signed for stops paying, pays late, or misses payments, your credit report can be negatively impacted.

Making Minimum Payments

Lenders who view your credit report don’t like to see that you are paying just the minimum payment. If you consistently pay the minimum payment due, it could indicate financial stress or confirm that you are unable to pay off the full balance.

]]>