stone’s throw from Bayview Beach this property offers an abundance of possibilities. With over 3,500 sq. feet you could continue to use it as the current owners do as an income producing vacation rental or convert it to a single family home or live in one side and rent the other!

There are gleaming hardwood floors throughout. The home offers two kitchens, both of which offer  granite counter tops. One side of this multi-family home offers a private master with office/sitting area on the second floor with a full bath. Enjoy watching your favorite team or program from the entertainment room with a gas fireplace. The three exterior decks are the perfect places to take in the Cape Cod air and enjoy the sea breezes off of the Bay!

granite counter tops. One side of this multi-family home offers a private master with office/sitting area on the second floor with a full bath. Enjoy watching your favorite team or program from the entertainment room with a gas fireplace. The three exterior decks are the perfect places to take in the Cape Cod air and enjoy the sea breezes off of the Bay!

This home boasts a strong rental history and the furnishings are negotiable. Enjoy all that Dennis Village has to offer including Golf, shops, restaurants and Mayflower Beach all within minutes from the home! Call Foran Realty today for more information about this water view multi-family home listed at only $1,350,000!

This home boasts a strong rental history and the furnishings are negotiable. Enjoy all that Dennis Village has to offer including Golf, shops, restaurants and Mayflower Beach all within minutes from the home! Call Foran Realty today for more information about this water view multi-family home listed at only $1,350,000!

![]() ]]>

]]>

Moving Can Be Stressful

60 Days Before You Move

- Sort and Purge-Go through every room, decide what needs to come with you and what can go. Make piles of things to throw away and things to donate.

- Plan a Yard Sale-Start planning a yard sale to reduce the amount of stuff you need to move. Some extra money for the move will also come in handy.

- Hire a Mover-Contact at least three moving companies. On-site estimates are better than over the phone or internet estimates. Get each estimate in writing, and make sure it has a USDOT (U.S. Department of Transportation) number on it.

- Create a Moving Binder-Store all of your move-related paperwork (checklists, contracts, receipts) in a binder. You may also want to inventory all of your items with photos or lists.

- Get Packing Supplies-Determine how many packing supplies you’ll need and designate a room where you can begin to store and organize.

- Take Measurements-If possible get room dimensions of your new home. Make sure large pieces of furniture will fit. Don’t forget to take measurements for appliances too.

- Confirm with Mover-Check with your mover the details of your move.

- Start Packing-Begin packing out-of-season clothes and unnecessary items.

- Label-Make sure to label boxes with what rooms the boxes will go in at your new home.

- Start/Stop Utilities-Make arrangements to connect and disconnect your cable, internet and utilities.

- Change your Address- Contact or visit your local Post Office to obtain a Change of Address form. You can also obtain this form online at http://www.usps.com.

- Make Notifications- Change your address to the following: registry of motor vehicles, banks, schools, friends & family, insurance companies, doctors and specialists, cell phone providers, credit card companies and magazine and newspapers.

- Contact Service Providers—Notify landscapers, cleaning services that you are moving, and look for new ones in your new hometown.

- Call Locksmith- Have your new home’s locks changed on moving day or before.

- Arrange Services- Have a cleaning company prepare the new home before you arrive and tidy the old home after you leave. Arrange for carpet cleaning too.

- Pack the bulk of your items.

- Start Cleaning-Begin cleaning any rooms in your house that have been emptied, such as closets, basements or attics.

- Pack Suitcases- Finish your general packing a few days before your moving date. Pack suitcases for everyone in the family with enough clothes to wear for a few days.

- Gather Keys- Organize all keys, alarm codes and garage door openers so that you can be prepared to hand them over to the new owner or real estate agent.

- Defrost the Freezer- Empty, clean and defrost the freezer at least 24 hours before moving day.

- Make Payment Plans- You will need to make sure you have made arrangements to pay the mover and have a tip (usually 10%-15%).

- List Contact Info- Write out a list for your movers of things they’ll need: phone numbers, exact moving address and maps.

- Take Inventory- Before the movers leave, sign the bill of lading/inventory list and keep a copy.

- Walk-Through- Do a walk-through of your new home with your real estate agent.

- Layout New Home- Tape names to doors to assist movers in placing furniture and boxes.

- Have Director- Arrange for someone to direct the movers at your new home.

How NOT to Negotiate a Home Purchase

When you are looking at buying a home there are don’ts you should be aware of. Many times the handling of the negotiation can mean the difference in huge amounts of money. This is why it is vital to have an experienced agent on your side. Here are just a few common pitfalls to avoid.

Not doing your homework

Doing your homework is important in such a large purchase. Ask your agent for a list of comparable homes recent sale prices. Look to see how long comparable listings have been on the market and what the average sale to list price ratio is. This will give you the information you need when making an offer and negotiating a final sale price.

Not understanding the seller

Try to look at the deal from the opposite side of the table. A sale is typically emotional for a seller. When making an offer try not to insult the seller, offering a fair and realistic offer to purchase will typically get you further in the negotiations. If you know the seller’s motivations for selling you may also be able to offer terms that might be more attractive like a quick close or inspection.

Showing your cards

While you want to know as much about the seller as possible divulge as little about yourself in the negotiation as possible. Any knowledge the seller has about your motivation can be used as leverage in the negotiation.

Getting your heart set

Buying a home can often be an emotional process. Identify several properties you’d be happy with as well. Be careful not to get your heart in the way of your head as it can sometimes hinder the deal.

Trying to win

In a sale there needs to be two ingredients: a seller who wants to sell and a buyer who wants to buy. Try not to getting caught up in the game. Ultimately it is about buying a home and not winning a negotiation.]]>

When you are looking at buying a home there are don’ts you should be aware of. Many times the handling of the negotiation can mean the difference in huge amounts of money. This is why it is vital to have an experienced agent on your side. Here are just a few common pitfalls to avoid.

Not doing your homework

Doing your homework is important in such a large purchase. Ask your agent for a list of comparable homes recent sale prices. Look to see how long comparable listings have been on the market and what the average sale to list price ratio is. This will give you the information you need when making an offer and negotiating a final sale price.

Not understanding the seller

Try to look at the deal from the opposite side of the table. A sale is typically emotional for a seller. When making an offer try not to insult the seller, offering a fair and realistic offer to purchase will typically get you further in the negotiations. If you know the seller’s motivations for selling you may also be able to offer terms that might be more attractive like a quick close or inspection.

Showing your cards

While you want to know as much about the seller as possible divulge as little about yourself in the negotiation as possible. Any knowledge the seller has about your motivation can be used as leverage in the negotiation.

Getting your heart set

Buying a home can often be an emotional process. Identify several properties you’d be happy with as well. Be careful not to get your heart in the way of your head as it can sometimes hinder the deal.

Trying to win

In a sale there needs to be two ingredients: a seller who wants to sell and a buyer who wants to buy. Try not to getting caught up in the game. Ultimately it is about buying a home and not winning a negotiation.]]>

Current Mortgage Rates!

What’s going to happen to mortgage rates in 2016? Lots of people, very smart people try to anticipate what is coming. We are well aware that they don’t always get it right, but the more we know the better prepared we can be.

Loan Rates Have Been Crazy!

A quick look at Freddie Mac’s history reveals that it has been more than five years since monthly average rates for 30-year fixed-rate mortgages (FRMs) topped 5 percent. At one point, at the end of 2012, they reached an all-time low of 3.35 percent. Right now they are still very close to that 3.35 percent and have yet to hit 4.

How quickly these low rates have become the norm! But don’t forget what normal used to be. If you look back over the decade before the housing and lending crisis really hit in 2008, the average annual rate for a fixed rate mortgage was over 6 percent for seven of the 10 years. In 2000, it was 8.05 percent. That sounds bad, but once again….remember the 80’s….. In 1981, the annual percentage rate average was more than twice that at 16.63 percent. Interest rates were above 10 percent from 1979 – 1990.

Don’t let those rates scare you. I have yet to find an economist that expects mortgage rates to rise to those levels again anytime in the near future.

So When Will “Normal” Return?

There are just too many variables to predict that with any accuracy at this point. The election, oil prices, stock activity and so much more can all make an impact and none of which at this point can accurately be predicted into the far future.

What Experts Forecast for 2016

Fannie Mae and the Mortgage Bankers Association (MBA) both have teams of economists dedicated to researching and forecasting trends in housing, including current mortgage rates.(Thank goodness for them…that means we can listen to what they say rather than doing our own research!)

The MBA team expects average rates for 30-year fixed rate mortgage to hit 5.1 percent in the last quarter of 2016. It anticipates fairly small  increases through 2016’s quarters: Q1 4.4 percent; Q2 4.7 percent; Q3 4.9 percent; Q4 5.1 percent.

Fannie Mae however forecasts much smaller rises in current mortgage rates with forecasts much smaller and shallower rises, with only 4.2 percent in the last quarter of 2016. Q1, 4.1 percent in Q2 and 4.2 percent in both Q3 and Q4.

So Who’s Right?

So we know that both of these research teams are incredibly intelligent and the fact is either could be right (or both could be wrong). Even the Federal Reserve will not confidently predict when its own rates will rise, and it sets those itself.

Most experts and economists currently expect to see some rises between now and the end of 2016. However, a few reckon it could be a long time before we get back to normal levels. One, Deutsche Bank equity strategist David Bianco, wrote in early October, “We see a better chance of landing men on Mars before a full normalization of nominal and real interest rates, especially 10-year yields, to historical norms.”

What to Watch For

Usually, good economic data causes rates to rise, while poor numbers pull the rates down. In particular, low unemployment and inflation at around 2 percent are important, because those are the main criteria the Fed looks at when setting its rates. But good numbers regarding gross domestic product (GDP), incomes, manufacturing, consumer confidence and spending, and so on are all likely to see rates rise sooner and faster. Poor ones generally have the opposite effect, as does bad news about foreign economies. What happened in Greece this past year definitely helped to keep our rates low!

increases through 2016’s quarters: Q1 4.4 percent; Q2 4.7 percent; Q3 4.9 percent; Q4 5.1 percent.

Fannie Mae however forecasts much smaller rises in current mortgage rates with forecasts much smaller and shallower rises, with only 4.2 percent in the last quarter of 2016. Q1, 4.1 percent in Q2 and 4.2 percent in both Q3 and Q4.

So Who’s Right?

So we know that both of these research teams are incredibly intelligent and the fact is either could be right (or both could be wrong). Even the Federal Reserve will not confidently predict when its own rates will rise, and it sets those itself.

Most experts and economists currently expect to see some rises between now and the end of 2016. However, a few reckon it could be a long time before we get back to normal levels. One, Deutsche Bank equity strategist David Bianco, wrote in early October, “We see a better chance of landing men on Mars before a full normalization of nominal and real interest rates, especially 10-year yields, to historical norms.”

What to Watch For

Usually, good economic data causes rates to rise, while poor numbers pull the rates down. In particular, low unemployment and inflation at around 2 percent are important, because those are the main criteria the Fed looks at when setting its rates. But good numbers regarding gross domestic product (GDP), incomes, manufacturing, consumer confidence and spending, and so on are all likely to see rates rise sooner and faster. Poor ones generally have the opposite effect, as does bad news about foreign economies. What happened in Greece this past year definitely helped to keep our rates low!

What’s going to happen to current mortgage rates in 2016? The short answer is nobody can be sure. If you’re reading this because you need to make an important decision (time the purchase of a home, perhaps, or decide when to refinance an adjustable rate mortgage, we haven’t been much help. However we have given you the signs to watch for!

Rates now are still low so it is a great time to buy a home and lock yourself in at those low fixed rates. The team at Foran Realty would be happy to help you with your home search needs on Cape Cod.

What’s going to happen to current mortgage rates in 2016? The short answer is nobody can be sure. If you’re reading this because you need to make an important decision (time the purchase of a home, perhaps, or decide when to refinance an adjustable rate mortgage, we haven’t been much help. However we have given you the signs to watch for!

Rates now are still low so it is a great time to buy a home and lock yourself in at those low fixed rates. The team at Foran Realty would be happy to help you with your home search needs on Cape Cod.

![]() https://www.lendingtree.com/mortgage-rates/mortgage-rates-what-to-expect-in-2016-article

]]>

https://www.lendingtree.com/mortgage-rates/mortgage-rates-what-to-expect-in-2016-article

]]>

Ready to be a homebuyer?

Have a checklist

Whether you are a 1st-time buyer or an experienced owner, buying a house requires a “preflight check,” in the words of Barry Zigas, director of housing policy for the Consumer Federation of America.

Read on for a checklist provided by Bankrate, including tips on the types of savings you need, plus advice about what matters beyond  purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

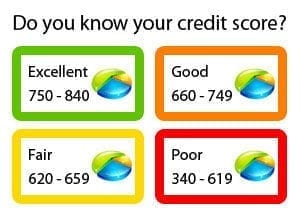

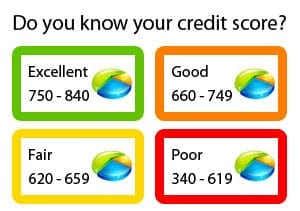

Strengthen Your Credit Score

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

purchasing a home at its resale value. And if you’re already ready to shop for a mortgage, find the best deal today by talking to your local lenders, mortgage brokers and researching online.

Strengthen Your Credit Score

“It’s a brave, new world with respect to credit requirements for mortgages,” says John Ulzheimer, credit expert and contributor at CreditSesame. One old rule still applies: The higher your credit score, the lower your monthly payments. “Below 660 or 680, you’re either going to have to pay sizable fees or a higher down payment,” Zigas says. And that’s pretty much the cutoff score for getting a mortgage, he says.

Higher scores wanted

Vicki Bott, a former official at the U.S. Department of Housing and Urban Development, says that her office noticed much the same thing. “While there are many qualified borrowers in the 580 range, the market today is probably looking for 640 to 660, at a minimum.” On the other end, a score of 700 to 720 will get you a good deal, and 750 and above will garner the best rates on the market. Improve your chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

chances by: pulling your credit reports and ensuring you’re not being unfairly penalized for old, paid or settled debts, Zigas says.

Stop applying for new credit a year before you apply for your mortgage. And keep that same policy in place until after you close on your home. A change in your score right before closing could adversely affect your mortgage approval.

Figure Out What You Can Afford

The buyer’s mantra should be: Get a home that’s financially comfortable. There are various rules of thumb that will help you get an idea of how much home you can afford.

Realistic debt-to-income ratio

For conventional loans, a safe formula is that home expenses should not exceed 28 percent of your gross monthly income, says Susan Tiffany, director of personal finance information for adults for the Credit Union National Association. Improve your chances by: trying on that financial obligation long before you sign the mortgage papers, says Tiffany. Before you home shop calculate the mortgage payment (there are several online calculators available) for the home in your intended price range, along with the increased expenses (such as taxes, insurance and utilities). Then bank the difference between that and what you’re paying now. Not only does it allow you to build a nice nest egg, but it gives you a feel for the comfort level in those payments. Once you have submitted your formal mortgage application, limit your spending to what is absolutely necessary. Do not make any substantial purchases and this could put your mortgage approval in jeopardy. Save for Down Payment and Closing Costs Depending on your credit and financing, you’ll typically need to save enough money for a down payment, somewhere between 3 percent and 20 percent of the home’s price.Don’t forget loan fees

Another substantial cash expense is your closing costs. Whatever your loan source, you’ll also need money to pay closing costs. For a $200,000 mortgage, closing costs run (depending on where you live) from $2,300 to $4,000. In a buyer’s market, you can also try to negotiate to have the seller pay a portion of the closing costs. Build a Healthy Savings Account Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years.

Building your savings is something you should do over and above saving money for the down payment and closing. Your lender wants to see that you’re not living paycheck to paycheck. If you have 3 to 5 months’ worth of mortgage payments set aside, that makes you a much better loan candidate. That money will also help cover maintenance and repair issues that come up when you own a home. While repairs are sporadic, items such as a new roof, water heater or other big-ticket items can hit suddenly and hard.

Get Preapproved for Your Mortgage

For serious home shoppers, “the No. 1 thing is they better have everything in order,” says Dick Gaylord, broker with Re/Max Real Estate Specialists in Long Beach, California, and former president of the National Association of Realtors. That means that before the real home shopping begins; you want to be sure that you have your financing in place. The preapproval process is “much more extensive” than it was a few years ago, he says.

Buy a House You Like

If you’re buying today for yourself and your family, you want a home that will make you happy for the next few years. Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at: http://www.bankrate.com/finance/mortgages/]]>

Gone are the days when you could count on a quick sale, Tiffany says. And depending on how much you put down, and how much you have to shell out to sell and relocate, short-term ownership can be a pretty expensive proposition.

Information gathered from and more information available at: http://www.bankrate.com/finance/mortgages/]]>

10 Steps to Buying Your Dream Home

TransUnion. A low credit score may hurt your chances for getting the best interest rate, or getting financing at all. So get a copy of your reports and know your credit scores. Applying for credit, even if you don’t use it can also hurt your score, so try not to apply for any additional credit for at least 6 months before purchasing a home. Be sure to address any errors on your credit report and document any efforts that you have made to correct those errors as a mortgage officer will want that paperwork.

TransUnion. A low credit score may hurt your chances for getting the best interest rate, or getting financing at all. So get a copy of your reports and know your credit scores. Applying for credit, even if you don’t use it can also hurt your score, so try not to apply for any additional credit for at least 6 months before purchasing a home. Be sure to address any errors on your credit report and document any efforts that you have made to correct those errors as a mortgage officer will want that paperwork.- Save your pennies.You’ll need to come up with cash for your down payment and closing costs. Lenders

usually like to see a minimum 20% of the home’s price as a down payment. If you can put down more than that, the lender may be willing to approve a larger loan or provide you with a better interest rate. If you have less, there are various private and public agencies — including Fannie Mae, Freddie Mac, the Federal Housing Administration and the Department of Veterans Affairs that will provide low down payment mortgages through banks and mortgage companies. If you qualify, it’s possible to pay as little as 3% up front. Once you’ve considered the down payment, make sure you’ve got enough to cover fees and closing costs. These may include the appraisal fee, loan fees, attorney’s fees, inspection fees, and the cost of a title search. They can easily add up to $5,000 to $10,000 — and often run to 5% of the mortgage amount.

usually like to see a minimum 20% of the home’s price as a down payment. If you can put down more than that, the lender may be willing to approve a larger loan or provide you with a better interest rate. If you have less, there are various private and public agencies — including Fannie Mae, Freddie Mac, the Federal Housing Administration and the Department of Veterans Affairs that will provide low down payment mortgages through banks and mortgage companies. If you qualify, it’s possible to pay as little as 3% up front. Once you’ve considered the down payment, make sure you’ve got enough to cover fees and closing costs. These may include the appraisal fee, loan fees, attorney’s fees, inspection fees, and the cost of a title search. They can easily add up to $5,000 to $10,000 — and often run to 5% of the mortgage amount.

- Find an agent: Mostsellers will list their homes for sale through an agent. But be aware that those agents work for the seller, not you. You need a buyer’s agent. Get in touch with a Real Estate Agent that you are comfortable with and that can help you find the home that is best for your personal situation. A buyer’s agent has the same access to homes for sale that a seller’s agent does, but their loyalty lays with you not the seller. The agents at Foran Realty are always ready, willing and able to represent you as a buyer’s agent.

- Search for a home. Your first step here is to figure out what city or neighborhood you want to live in. Try also to get an idea about the real estate market in the area. For example, if homes are selling close to or even above the asking price, that indicates a desirable area. Consider house hunting in the off-season or during the colder months of the year. You’ll have less competition and sellers may be more willing to negotiate

- Make an offer. Once you find the house you want, it is time to make your bid. When working with a buyer’s broker, get advice from him or her on an initial offer. Try to line up comparable data on at least three houses that have sold recently in the area. If you really want the house, don’t lowball the offer. The seller may give up in disgust. Remember, that your leverage depends on the pace of the market. In a slow market, you’ve got muscle; in a hot market, you may have none at all. Once you reach an agreed upon price, the seller’s agent will draw up an offer to purchase that includes an estimated closing date (usually 45 to 60 days from acceptance of the offer).

- Enter contract. Have your buyer’s agent review this document to make sure the deal is contingent upon:

- Your obtaining a mortgage

- A home inspection that shows no significant defects

- A guarantee that you may conduct a walk-through inspection.

- Secure a loan.Now call your mortgage broker or lender and submit your formal mortgage application. Be sure to include the information from your preapproval as you want the process to be as streamlined as possible.

- Get an inspection: In addition to the appraisal that the mortgage lender will make of your home, you should hire your own home inspector. An inspection costs about $300, on average, and could cost up to $1,000. Be sure that you ask to be there during the inspection. This will allow you to learn a lot about your house. If the inspector turns up major problems, like a roof that needs to be replaced, then ask your buyer’s agent to discuss it with the seller. You will either want the seller to fix the problem before you move in, or deduct the cost of the repair from the final price. If the seller won’t agree to either remedy you may decide to walk away from the deal, which you can do without penalty as long as you have that contingency written into the contract.

- Close the deal. About a week before the actual closing, you will receive a Closing Statement from your lender

that lists all the charges you can expect to pay at closing. Review it carefully as it will detail all of the closing costs you will be required to pay at the closing. It should also detail all expenses that you have already paid including inspections, application fees etc. The actual closing is somewhat anticlimactic, but your buyer’s agent can brief you on the particulars.

that lists all the charges you can expect to pay at closing. Review it carefully as it will detail all of the closing costs you will be required to pay at the closing. It should also detail all expenses that you have already paid including inspections, application fees etc. The actual closing is somewhat anticlimactic, but your buyer’s agent can brief you on the particulars.

WBZ Radio and Patrick Foran – Dont Miss This Great Info About Renting Your Home!

WBZ Radio and Patrick Foran[/caption]

[embed]https://www.youtube.com/watch?v=hOGqBUUX68g[/embed]

Whether you are looking to purchase or rent a home Patrick Foran and the staff at Foran Realty can help you find exactly what you are looking for. Patrick Foran is also an accredited member of the National Home Watch Association and has been fully licensed to manage your property in the event that you are not available. Be sure to call Foran Realty today for additional information.]]>

WBZ Radio and Patrick Foran[/caption]

[embed]https://www.youtube.com/watch?v=hOGqBUUX68g[/embed]

Whether you are looking to purchase or rent a home Patrick Foran and the staff at Foran Realty can help you find exactly what you are looking for. Patrick Foran is also an accredited member of the National Home Watch Association and has been fully licensed to manage your property in the event that you are not available. Be sure to call Foran Realty today for additional information.]]>

Condo Considerations

Could condo living be for you? For many condominium living can be an attractive alternative to a single family home. The price per square foot of a condo is often less than a single family home. Before you make the leap to condo living make sure to do your homework to see if it truly is the best choice for you. Here is a checklist of a few things you may want to consider before signing on the dotted line.

Could condo living be for you? For many condominium living can be an attractive alternative to a single family home. The price per square foot of a condo is often less than a single family home. Before you make the leap to condo living make sure to do your homework to see if it truly is the best choice for you. Here is a checklist of a few things you may want to consider before signing on the dotted line.

- Condominiums have monthly maintenance fees.

- Check with the condominium association to see what the annual increase in the monthly maintenance fee has been for the past few years.

- What is the percentage of residents are current with their monthly association payments. Look for about ninety-seven percent of the development’s residents to be current with their monthly payments.

- What percentage of the association fees are dedicated to a reserve fund. A good number would be at least 10 percent of the association’s annual budget.

- What are the condition of the condo’s roof and major mechanical systems? When were they last replaced or repaired. When the condo requires big upgrades, costly “special assessment” fees are passed on to the homeowners.

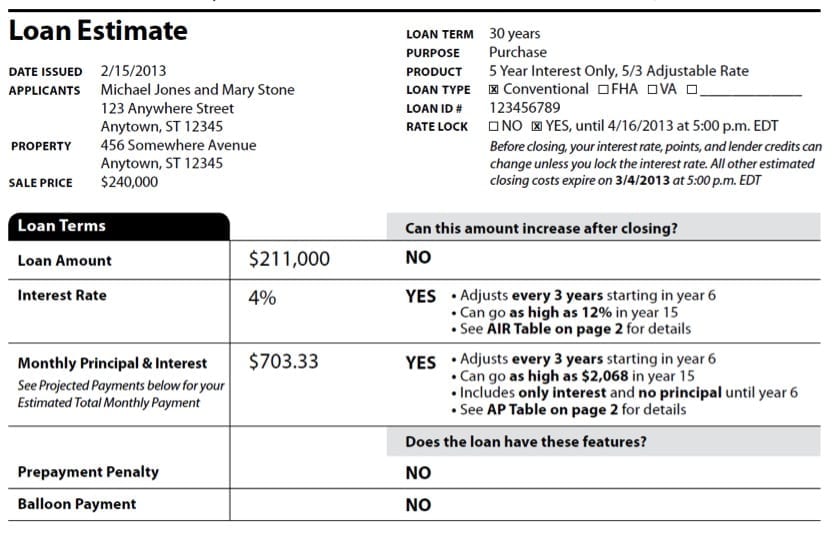

New Disclosure Regulations

paperwork that needed to be signed but made little to no sense to those of us signing it? Well that is hopefully being changed with the new disclosure regulations that went into effect October 3, 2015. The new rules, known as TRID, the new rules effect buyers and those that are refinancing will see two new documents: the Loan Estimate (LE) and the Closing Disclosure (CD) documents.

paperwork that needed to be signed but made little to no sense to those of us signing it? Well that is hopefully being changed with the new disclosure regulations that went into effect October 3, 2015. The new rules, known as TRID, the new rules effect buyers and those that are refinancing will see two new documents: the Loan Estimate (LE) and the Closing Disclosure (CD) documents.

Replacing the Good Faith Estimate and the early Truth-In-Lending statement (let’s be honest…that one never made any sense!) is the Loan Estimate (LE) Form This form summarizes the terms of a mortgage and estimates any and all loan fees and closing costs. The new form combines the original Good Faith Estimate with the early Truth-in-Lending statement into one shorter and hopefully easier to decipher document.

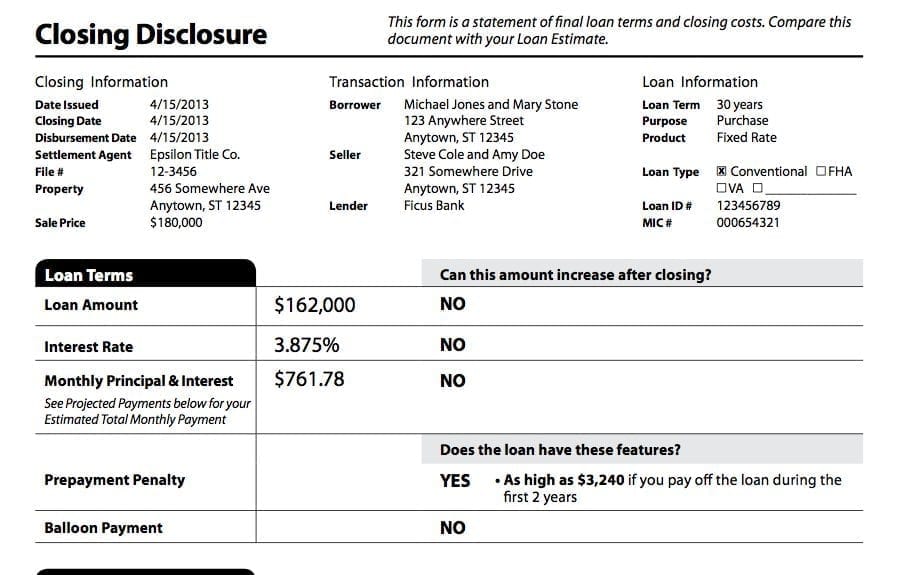

Replacing the final Truth-in-Lending statement and the HUD-1 settlement is the Closing Disclosure (CD)

Replacing the Good Faith Estimate and the early Truth-In-Lending statement (let’s be honest…that one never made any sense!) is the Loan Estimate (LE) Form This form summarizes the terms of a mortgage and estimates any and all loan fees and closing costs. The new form combines the original Good Faith Estimate with the early Truth-in-Lending statement into one shorter and hopefully easier to decipher document.

Replacing the final Truth-in-Lending statement and the HUD-1 settlement is the Closing Disclosure (CD) Form. This form provides a detailed account of the entire real estate transaction, including loan terms, fees and closing costs. The new document combines the Truth-in-Lending statement and the HUD-1 Settlement statement into a form that is shorter and more user-friendly. It’s easier for consumers to read.

“Fifteen years ago lenders and title companies weren’t held to their estimates of what a loan would cost, so occasionally you would hear horror stories of borrowers forced to pay an extra $5,000 at the closing table,” says Mark Dietz, senior vice president and area sales manager for EagleBank in Potomac. “Earlier revisions to transaction documents made it clear which fees could change and which ones couldn’t. These new revisions are taking clarity one step further, which is a good step to make consumers feel more confident that they understand their loan terms.”1

The experts that have worked diligently to create the updated forms say that the new documents are designed to make it easier for consumers to compare loan options as well as to understand and become aware if something changed between the time of loan application and settlement.

Form. This form provides a detailed account of the entire real estate transaction, including loan terms, fees and closing costs. The new document combines the Truth-in-Lending statement and the HUD-1 Settlement statement into a form that is shorter and more user-friendly. It’s easier for consumers to read.

“Fifteen years ago lenders and title companies weren’t held to their estimates of what a loan would cost, so occasionally you would hear horror stories of borrowers forced to pay an extra $5,000 at the closing table,” says Mark Dietz, senior vice president and area sales manager for EagleBank in Potomac. “Earlier revisions to transaction documents made it clear which fees could change and which ones couldn’t. These new revisions are taking clarity one step further, which is a good step to make consumers feel more confident that they understand their loan terms.”1

The experts that have worked diligently to create the updated forms say that the new documents are designed to make it easier for consumers to compare loan options as well as to understand and become aware if something changed between the time of loan application and settlement.

If you buying a home, be sure that your lender provides you with the documentation that you need to make the process a seamless one. Review the documents with your Realtor to ensure that the fees are the norm and that there isn’t anything that you should be concerned about. You should also be aware of new time lines for disclosure requirements. Deals that used to close in 30 – 45 days you should now plan for 45 – 60 days. It is imperative that work with you lender closely to get the necessary paperwork and supporting documents to them in a timely manner, delays could cause a delay in your closing!

Your friends at Foran Realty can help you find a lender and help guide you through the new process.

If you buying a home, be sure that your lender provides you with the documentation that you need to make the process a seamless one. Review the documents with your Realtor to ensure that the fees are the norm and that there isn’t anything that you should be concerned about. You should also be aware of new time lines for disclosure requirements. Deals that used to close in 30 – 45 days you should now plan for 45 – 60 days. It is imperative that work with you lender closely to get the necessary paperwork and supporting documents to them in a timely manner, delays could cause a delay in your closing!

Your friends at Foran Realty can help you find a lender and help guide you through the new process.

![]() 1 https://www.washingtonpost.com/realestate/]]>

1 https://www.washingtonpost.com/realestate/]]>

The Love Letter is Back

The love letter is back! What is a love letter in real estate? When the market is hot and competition for desirable homes is high buyers can gain an advantage by writing the seller a love letter.

You may be wondering why in the world would I write a love letter to a seller? The answer: you want an advantage in a competitive real estate market.

What should I put in my love letter?

Compliment the seller on their home

Tell the seller why you love the home

Compliment the neighborhood

Make it personal

Be genuine

Love letters often appeal to a seller’s emotions and often especially if the owner has lived in the home a while the decision to sell a home is a very emotional process. If you find yourself in a bidding war or want to land the perfect home it may be a love letter that makes all the difference.

]]>

The love letter is back! What is a love letter in real estate? When the market is hot and competition for desirable homes is high buyers can gain an advantage by writing the seller a love letter.

You may be wondering why in the world would I write a love letter to a seller? The answer: you want an advantage in a competitive real estate market.

What should I put in my love letter?

Compliment the seller on their home

Tell the seller why you love the home

Compliment the neighborhood

Make it personal

Be genuine

Love letters often appeal to a seller’s emotions and often especially if the owner has lived in the home a while the decision to sell a home is a very emotional process. If you find yourself in a bidding war or want to land the perfect home it may be a love letter that makes all the difference.

]]>