paperwork that needed to be signed but made little to no sense to those of us signing it? Well that is hopefully being changed with the new disclosure regulations that went into effect October 3, 2015. The new rules, known as TRID, the new rules effect buyers and those that are refinancing will see two new documents: the Loan Estimate (LE) and the Closing Disclosure (CD) documents.

paperwork that needed to be signed but made little to no sense to those of us signing it? Well that is hopefully being changed with the new disclosure regulations that went into effect October 3, 2015. The new rules, known as TRID, the new rules effect buyers and those that are refinancing will see two new documents: the Loan Estimate (LE) and the Closing Disclosure (CD) documents.

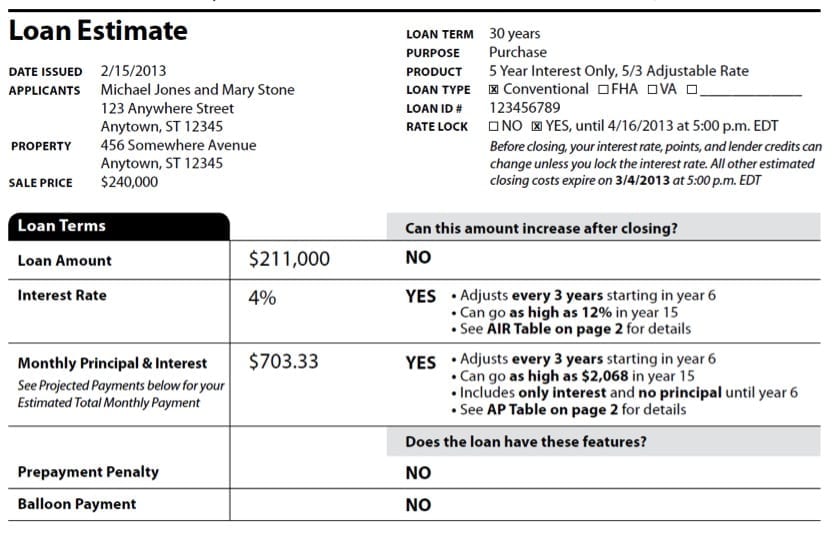

Replacing the Good Faith Estimate and the early Truth-In-Lending statement (let’s be honest…that one never made any sense!) is the Loan Estimate (LE) Form This form summarizes the terms of a mortgage and estimates any and all loan fees and closing costs. The new form combines the original Good Faith Estimate with the early Truth-in-Lending statement into one shorter and hopefully easier to decipher document.

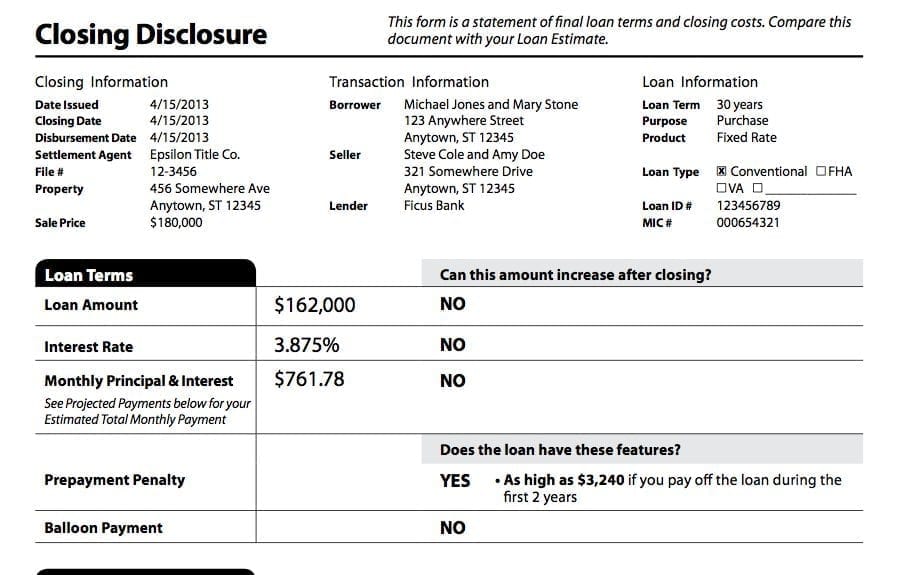

Replacing the final Truth-in-Lending statement and the HUD-1 settlement is the Closing Disclosure (CD)

Replacing the Good Faith Estimate and the early Truth-In-Lending statement (let’s be honest…that one never made any sense!) is the Loan Estimate (LE) Form This form summarizes the terms of a mortgage and estimates any and all loan fees and closing costs. The new form combines the original Good Faith Estimate with the early Truth-in-Lending statement into one shorter and hopefully easier to decipher document.

Replacing the final Truth-in-Lending statement and the HUD-1 settlement is the Closing Disclosure (CD) Form. This form provides a detailed account of the entire real estate transaction, including loan terms, fees and closing costs. The new document combines the Truth-in-Lending statement and the HUD-1 Settlement statement into a form that is shorter and more user-friendly. It’s easier for consumers to read.

“Fifteen years ago lenders and title companies weren’t held to their estimates of what a loan would cost, so occasionally you would hear horror stories of borrowers forced to pay an extra $5,000 at the closing table,” says Mark Dietz, senior vice president and area sales manager for EagleBank in Potomac. “Earlier revisions to transaction documents made it clear which fees could change and which ones couldn’t. These new revisions are taking clarity one step further, which is a good step to make consumers feel more confident that they understand their loan terms.”1

The experts that have worked diligently to create the updated forms say that the new documents are designed to make it easier for consumers to compare loan options as well as to understand and become aware if something changed between the time of loan application and settlement.

Form. This form provides a detailed account of the entire real estate transaction, including loan terms, fees and closing costs. The new document combines the Truth-in-Lending statement and the HUD-1 Settlement statement into a form that is shorter and more user-friendly. It’s easier for consumers to read.

“Fifteen years ago lenders and title companies weren’t held to their estimates of what a loan would cost, so occasionally you would hear horror stories of borrowers forced to pay an extra $5,000 at the closing table,” says Mark Dietz, senior vice president and area sales manager for EagleBank in Potomac. “Earlier revisions to transaction documents made it clear which fees could change and which ones couldn’t. These new revisions are taking clarity one step further, which is a good step to make consumers feel more confident that they understand their loan terms.”1

The experts that have worked diligently to create the updated forms say that the new documents are designed to make it easier for consumers to compare loan options as well as to understand and become aware if something changed between the time of loan application and settlement.

If you buying a home, be sure that your lender provides you with the documentation that you need to make the process a seamless one. Review the documents with your Realtor to ensure that the fees are the norm and that there isn’t anything that you should be concerned about. You should also be aware of new time lines for disclosure requirements. Deals that used to close in 30 – 45 days you should now plan for 45 – 60 days. It is imperative that work with you lender closely to get the necessary paperwork and supporting documents to them in a timely manner, delays could cause a delay in your closing!

Your friends at Foran Realty can help you find a lender and help guide you through the new process.

If you buying a home, be sure that your lender provides you with the documentation that you need to make the process a seamless one. Review the documents with your Realtor to ensure that the fees are the norm and that there isn’t anything that you should be concerned about. You should also be aware of new time lines for disclosure requirements. Deals that used to close in 30 – 45 days you should now plan for 45 – 60 days. It is imperative that work with you lender closely to get the necessary paperwork and supporting documents to them in a timely manner, delays could cause a delay in your closing!

Your friends at Foran Realty can help you find a lender and help guide you through the new process.

![]() 1 https://www.washingtonpost.com/realestate/]]>

1 https://www.washingtonpost.com/realestate/]]>